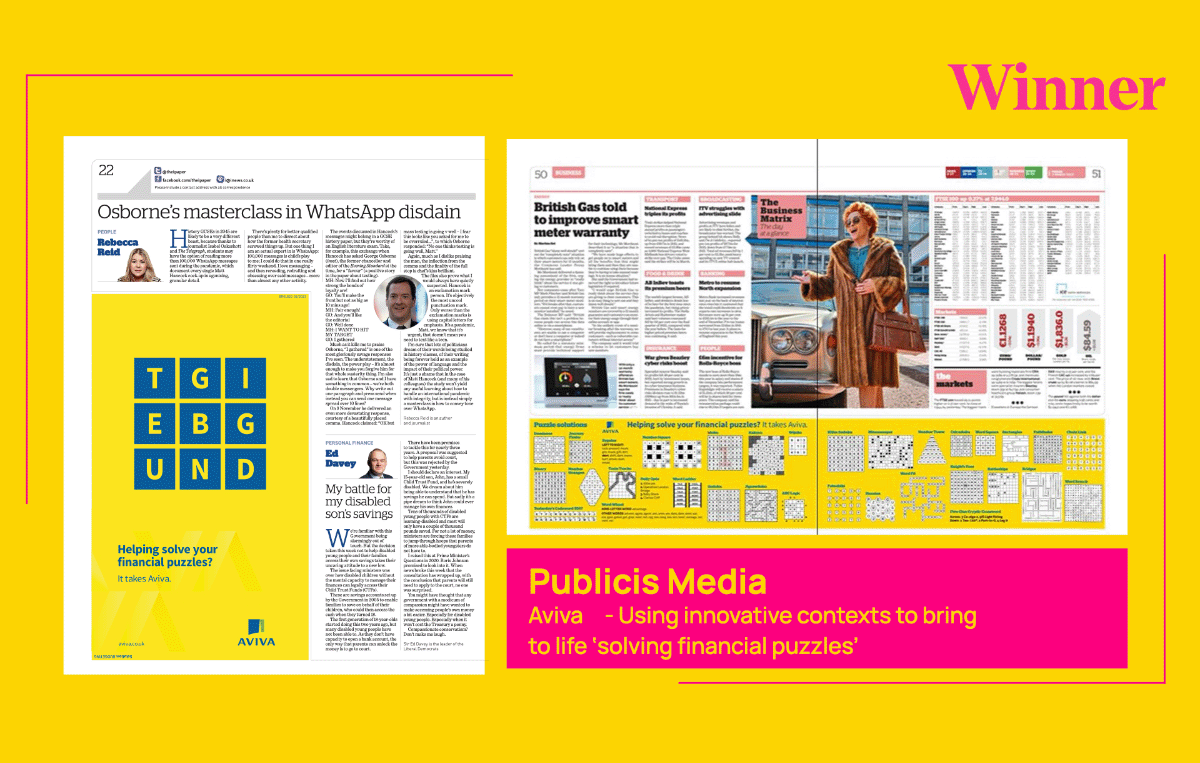

Aviva – Innovative contexts help solve financial puzzles

Publicis Media – Aviva

Newsworks

Because Journalism Matters

These case studies showcase the best examples of advertising across print and digital news brands. Each campaign below demonstrates how news brands were used to deliver one of six communication roles:

Address an issue: focus on a specific issue or event

Change minds: change consumer opinion of a brand

Fame & stature: create the sense of brand momentum

Build trust: consolidate or develop a brand's reputation

Education & understanding: develop consumer understanding of a brand

Prompt action: cause consumer action, directly or indirectly impacting sales

You can search for a specific case study using the search icon in the navigation. Alternatively you can filter campaigns by objective or category.

Publicis Media – Aviva

Spark Foundry – Asda

Bicycle London – Sarson’s

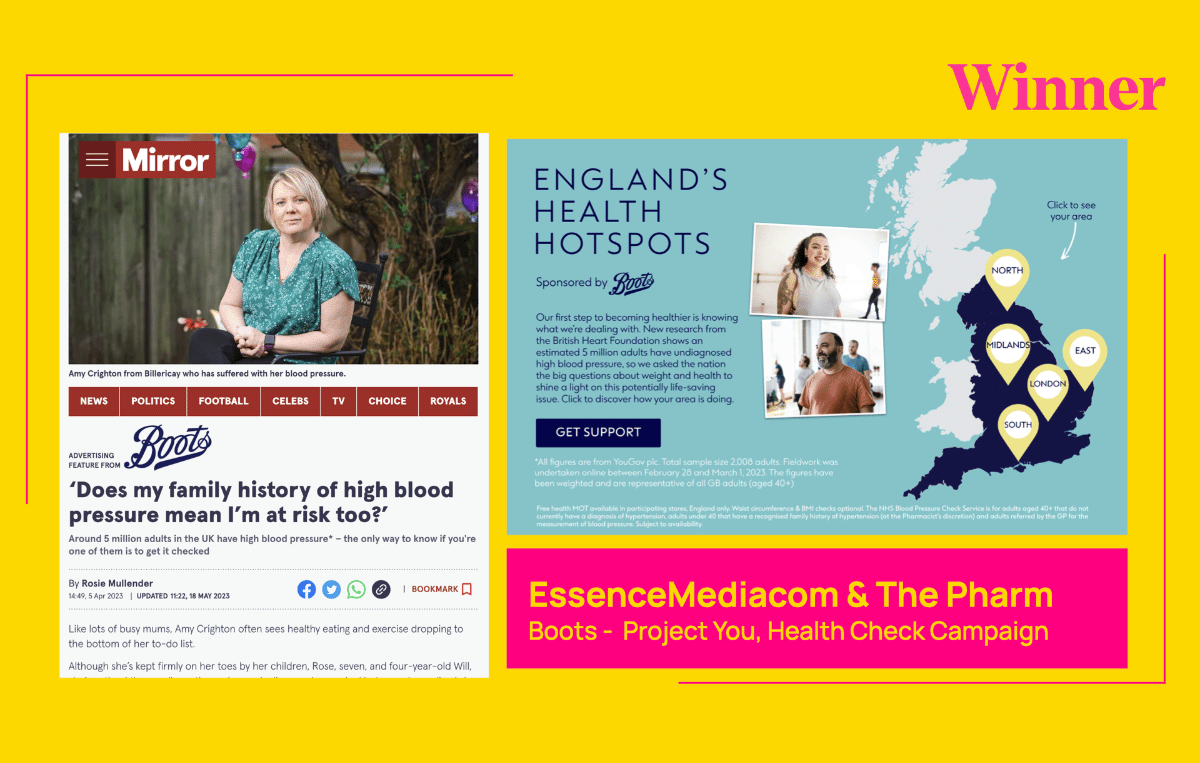

EssenceMediacom & The Pharm – Boots

Zenith – Scottish Widows

Spark Foundry – Asda

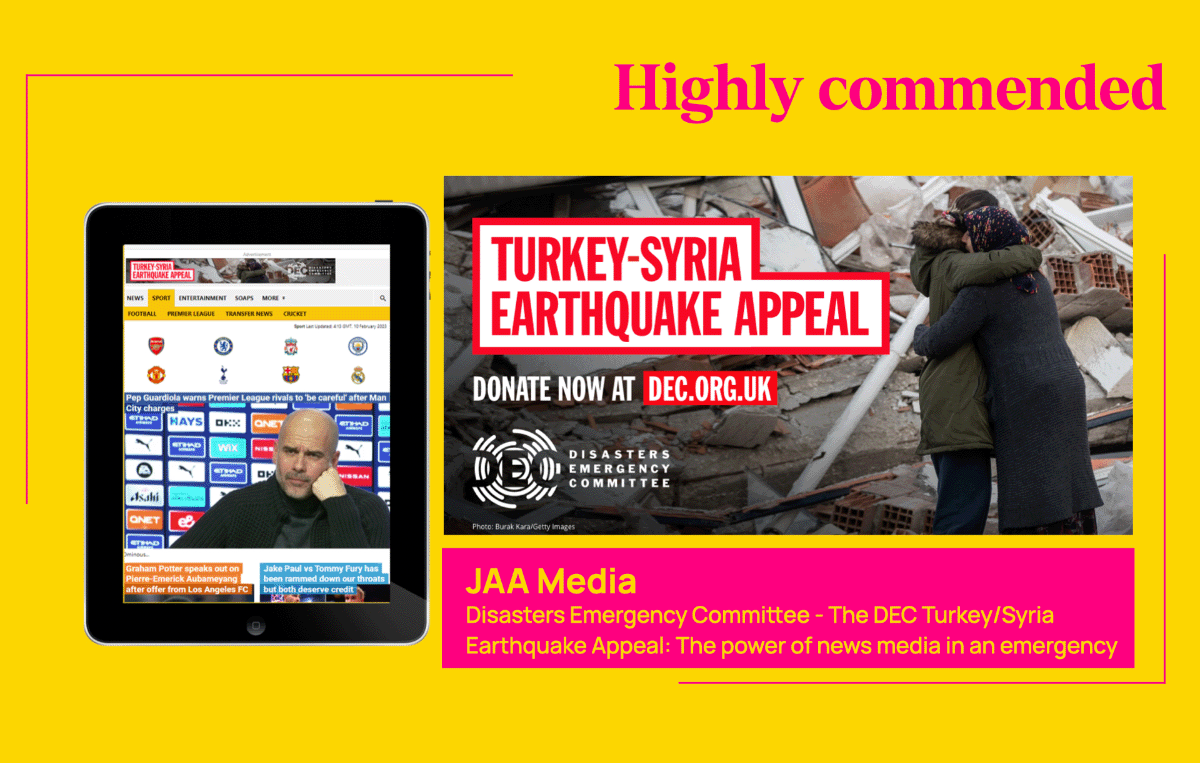

JAA – Disasters Emergency Committee

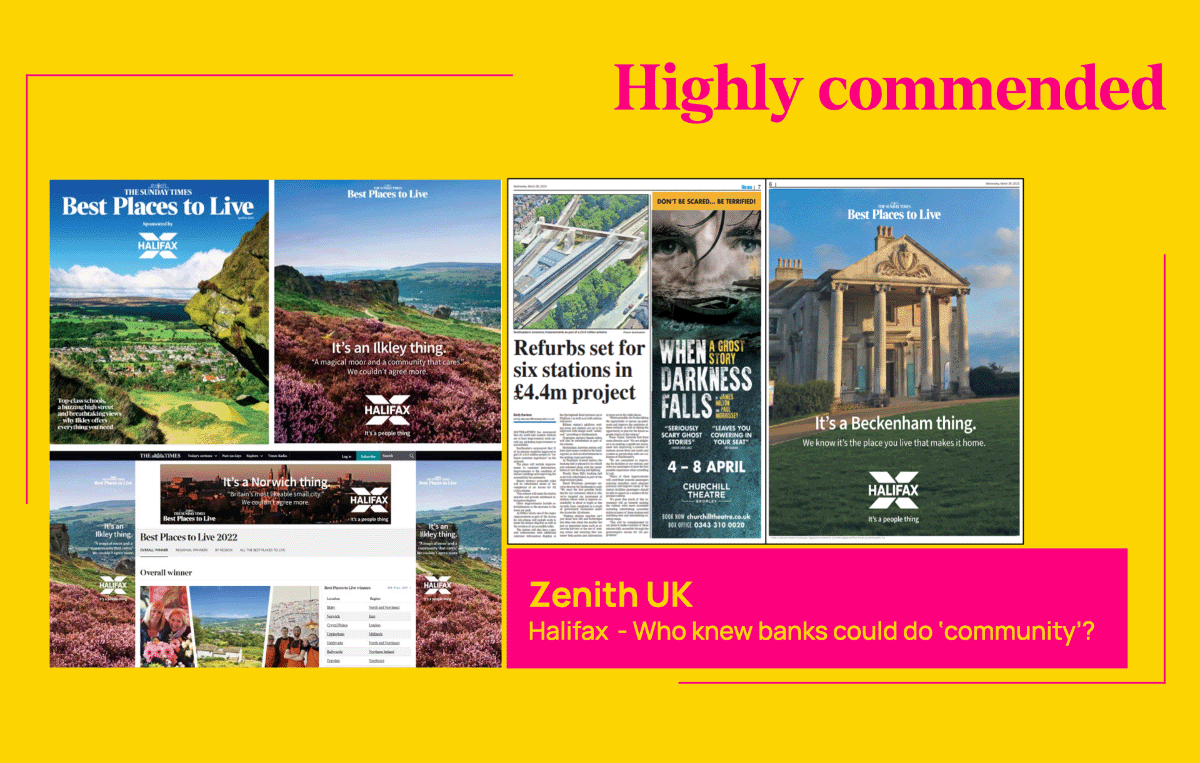

Zenith – Halifax

OmniGov @ MGOMD – GambleAware